| |

|

Bitcoin Affairs Premium

|

|

Weekly

|

|

Deep Dive

|

|

|

|

No. 001 · 6 Jul 2026

|

Over the past few days, Bitcoin has bounced from around $58k to $63k, and much of Bitcoin Twitter is calling the bottom in. Is this the real cycle low, or is it a mid-cycle head fake before another leg down?

In today’s Weekly Deep Dive, we look at some of the most important on-chain metrics that have always marked past cycle tops and bottoms. We will then zoom out to the macro backdrop and the long-term structural picture to see if we can actually answer this million-dollar question.

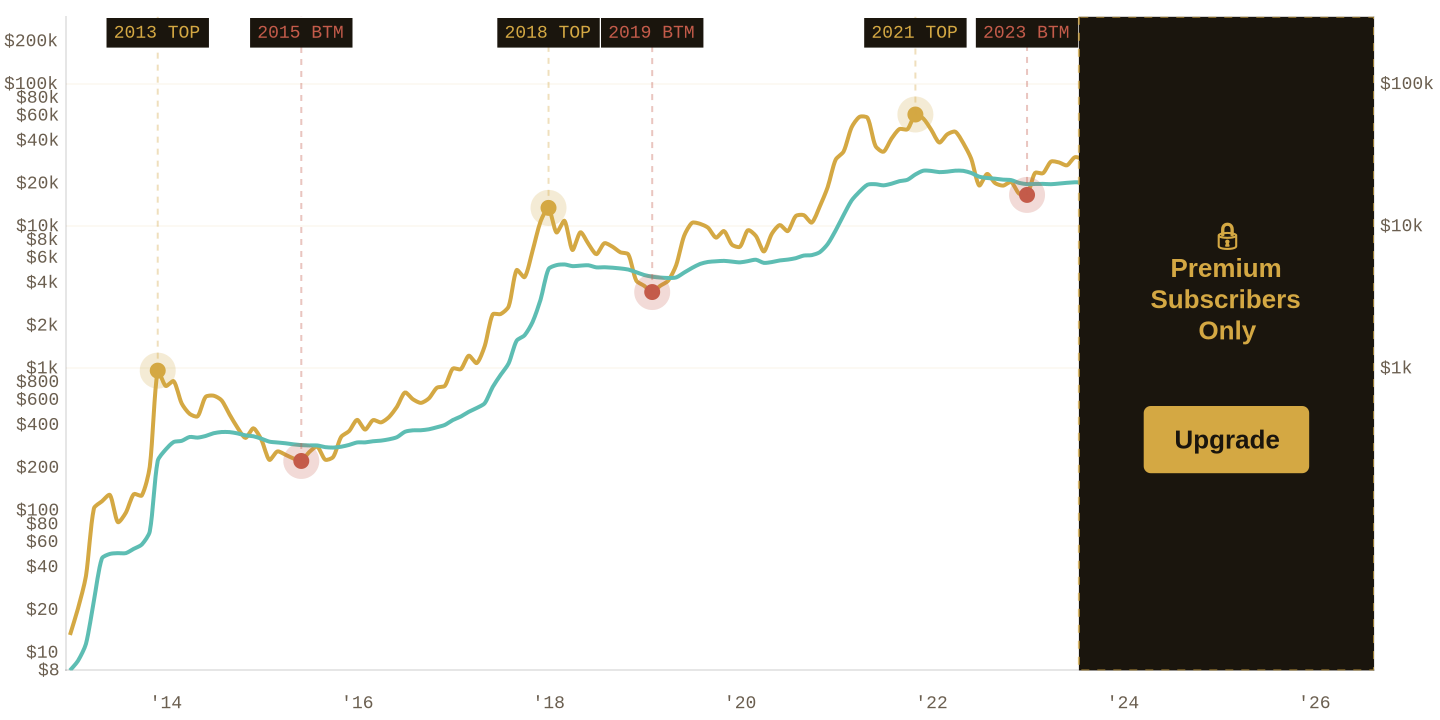

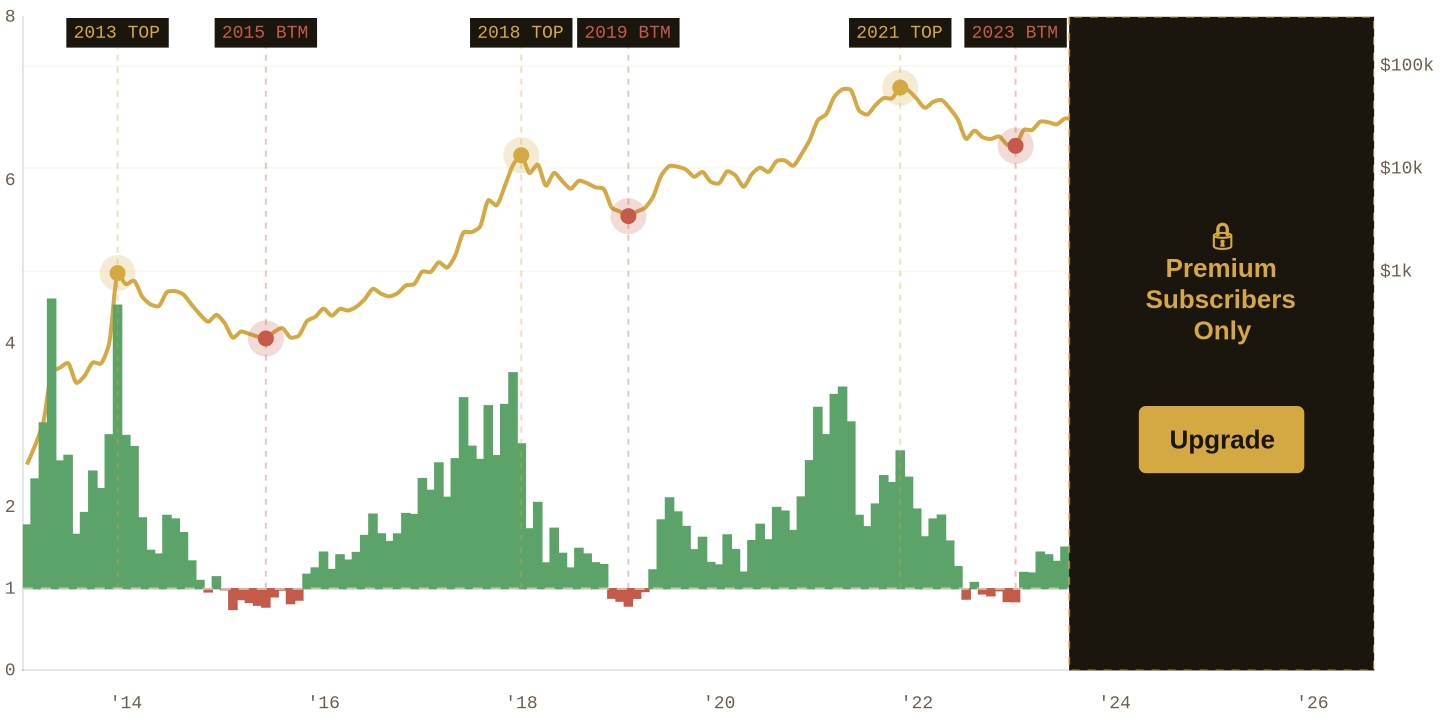

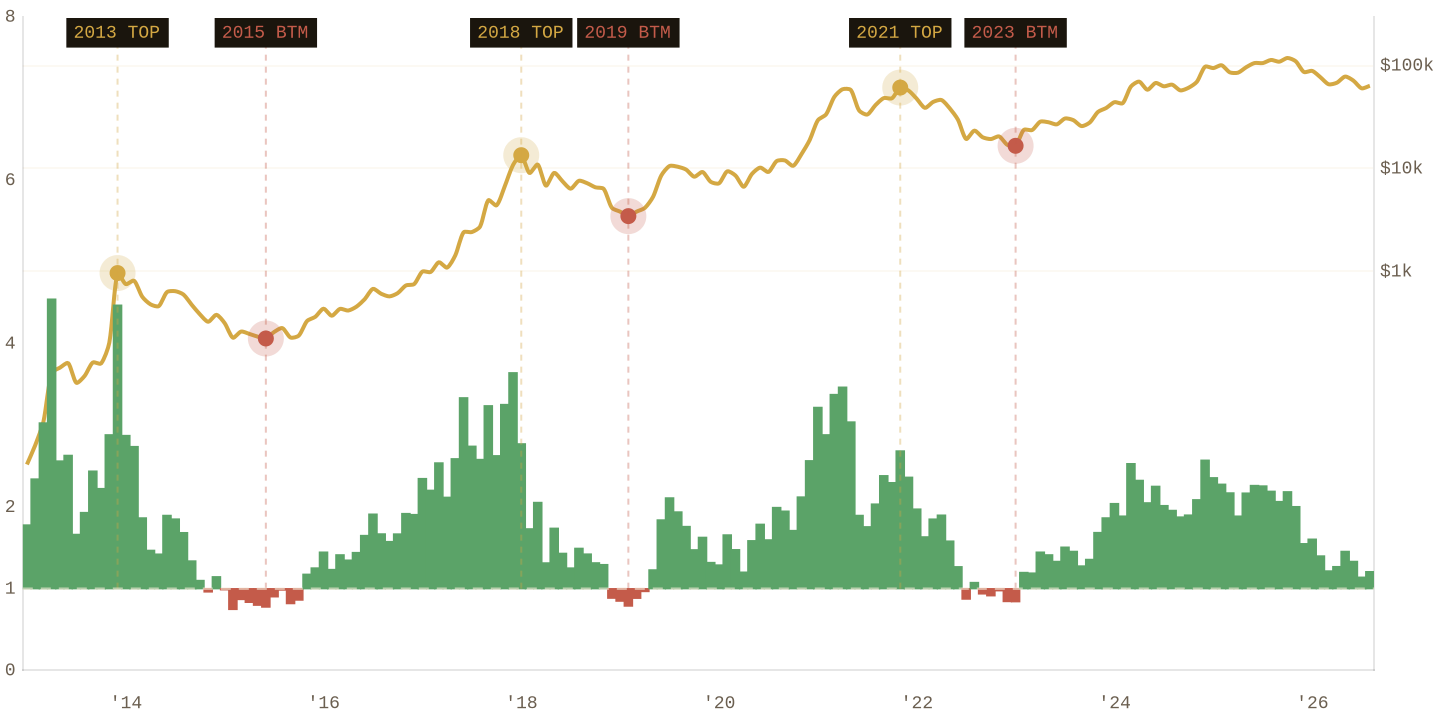

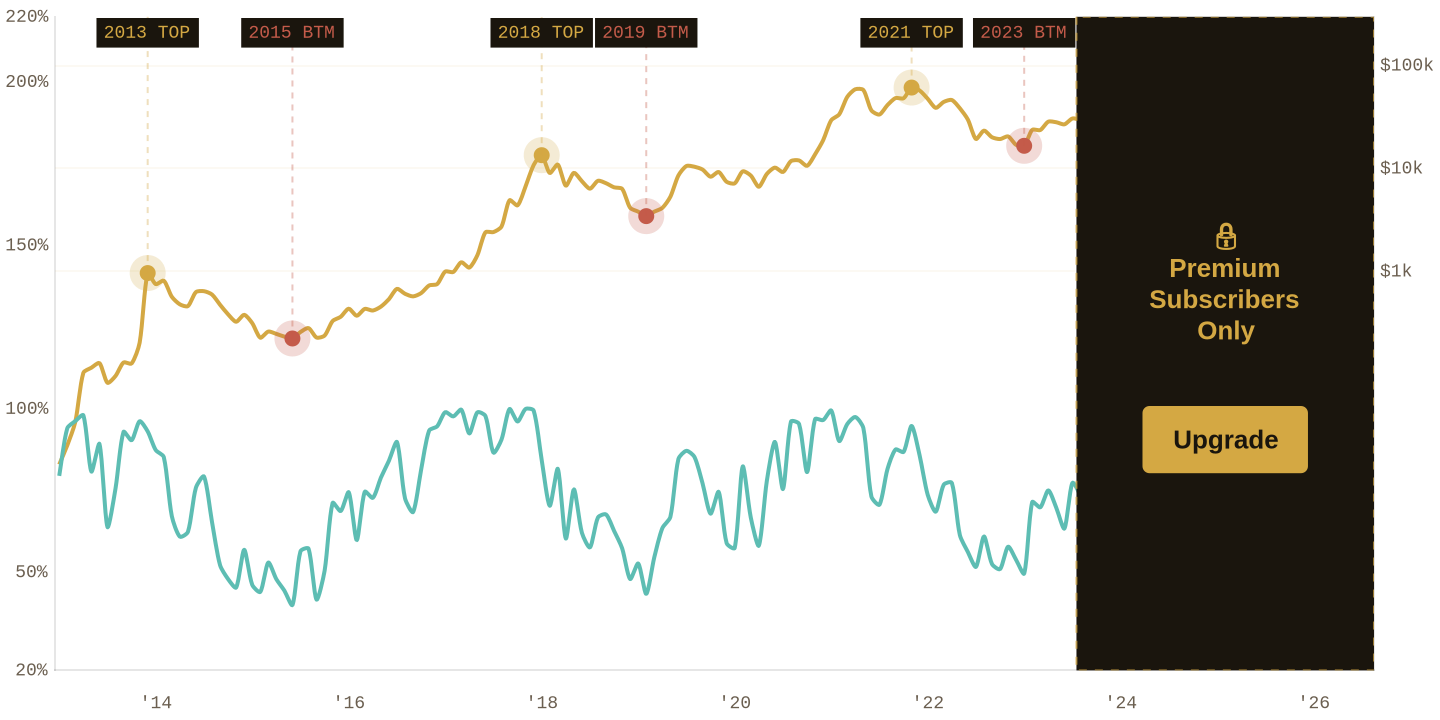

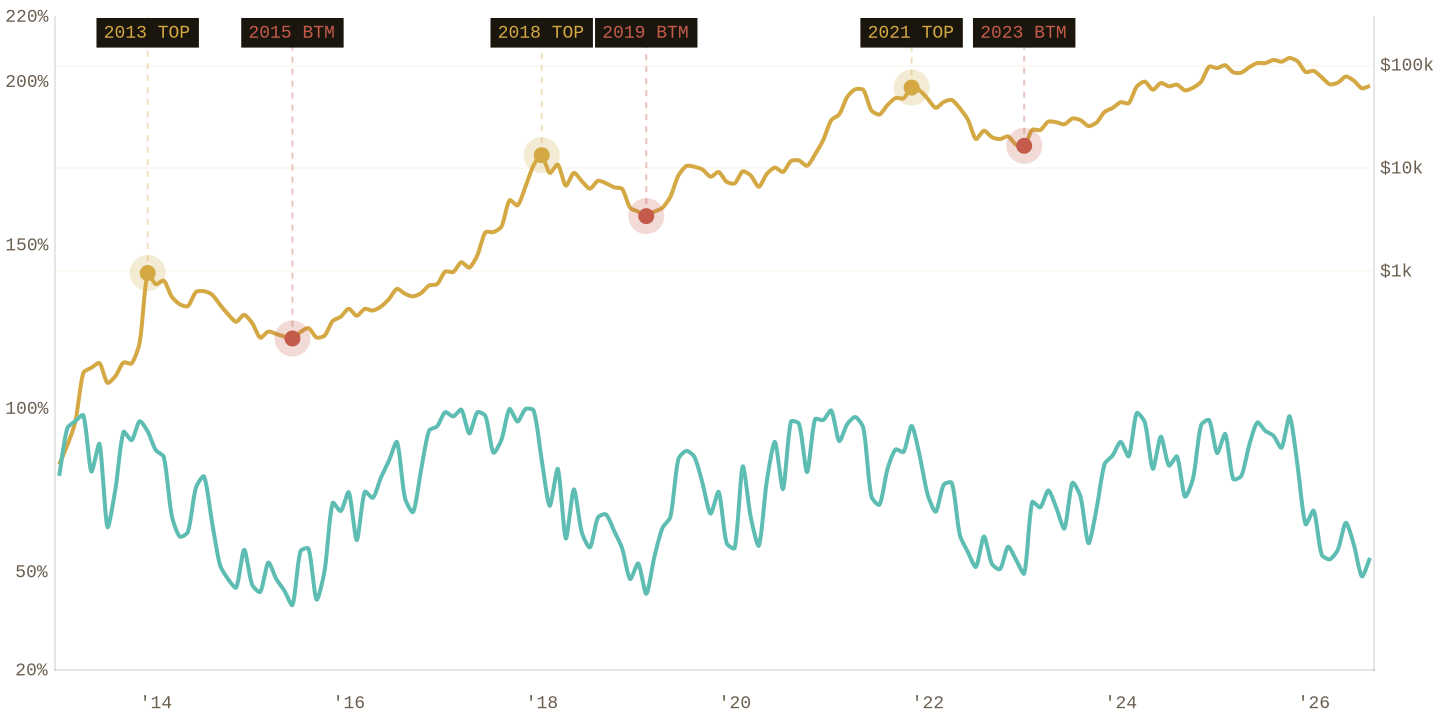

Realized Price is the average on-chain acquisition cost of every Bitcoin in circulation, weighted by when each coin last moved. Think of it as the network's aggregate cost basis. Historically, cycle bottoms print when spot price falls below realized price, meaning the average holder is underwater. In the 2015, 2018, and 2022 bottoms, spot spent multiple weeks trading below realized price.

The current realized price is 🔒 upgrade to unlock which is 🔒 upgrade to unlock the current price of $62,752.

|

|

BTC Price (log) Realized Price

|

|

|

|

BTC Price (log) Realized Price

|

|

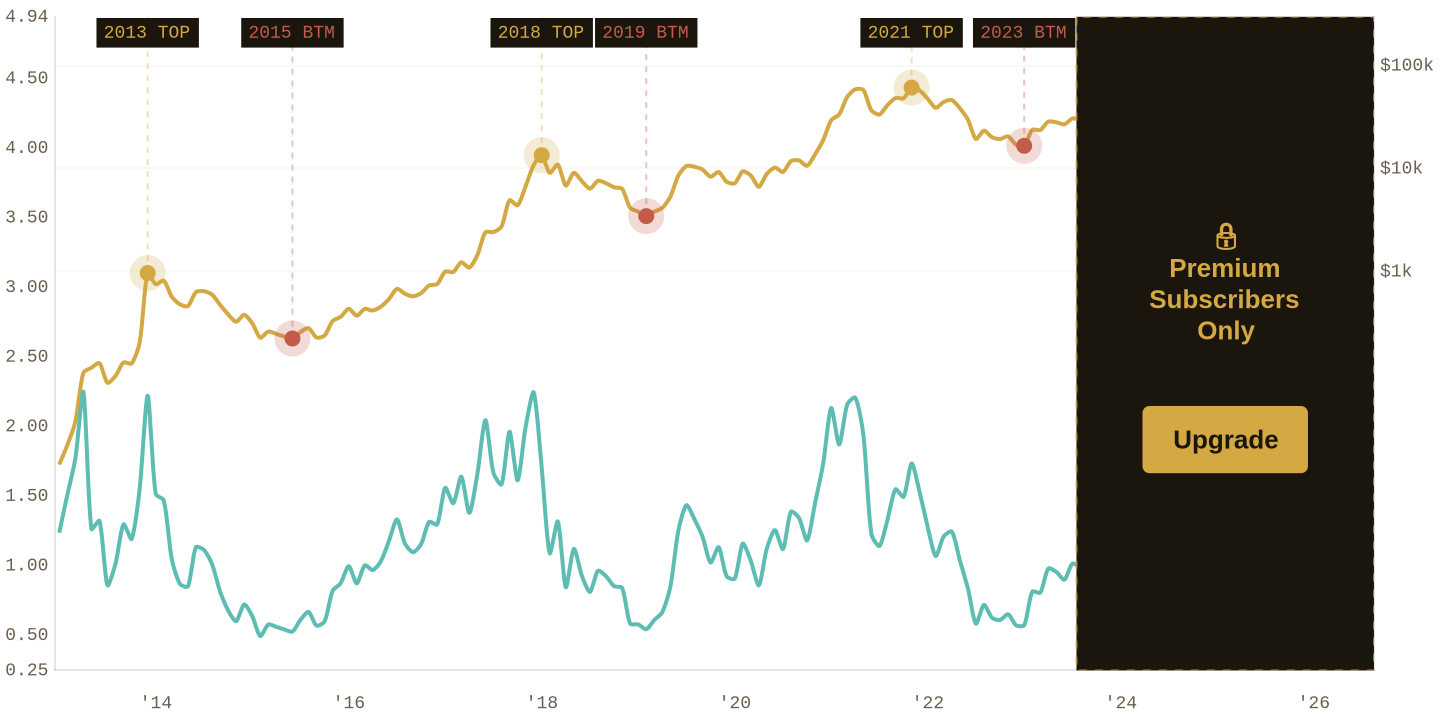

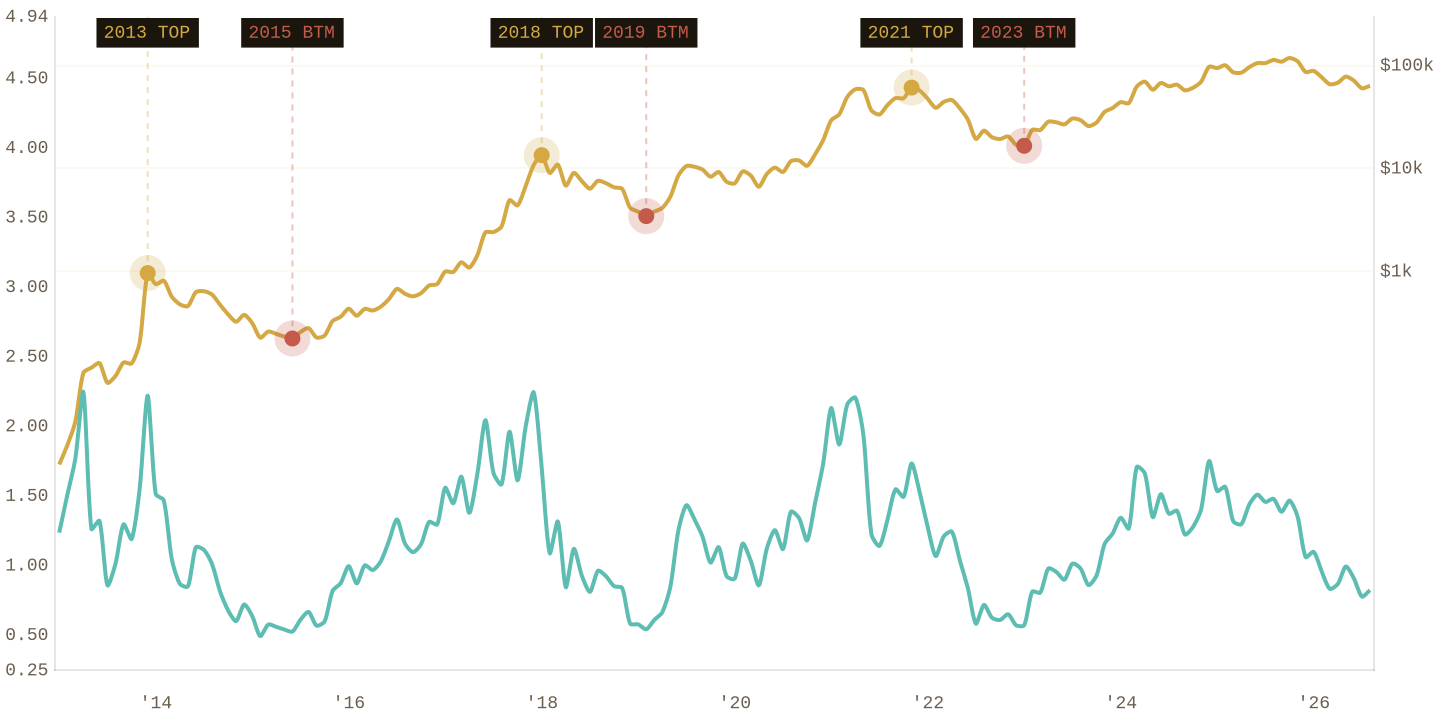

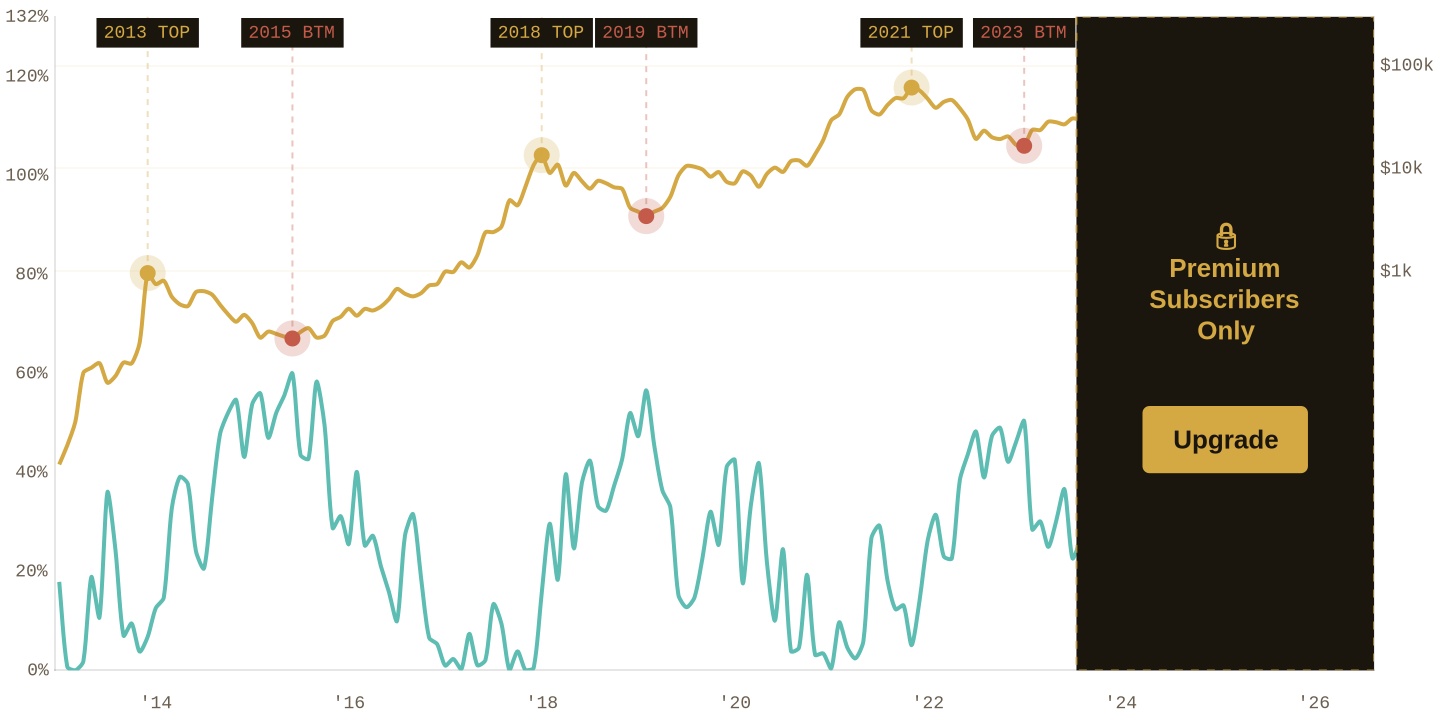

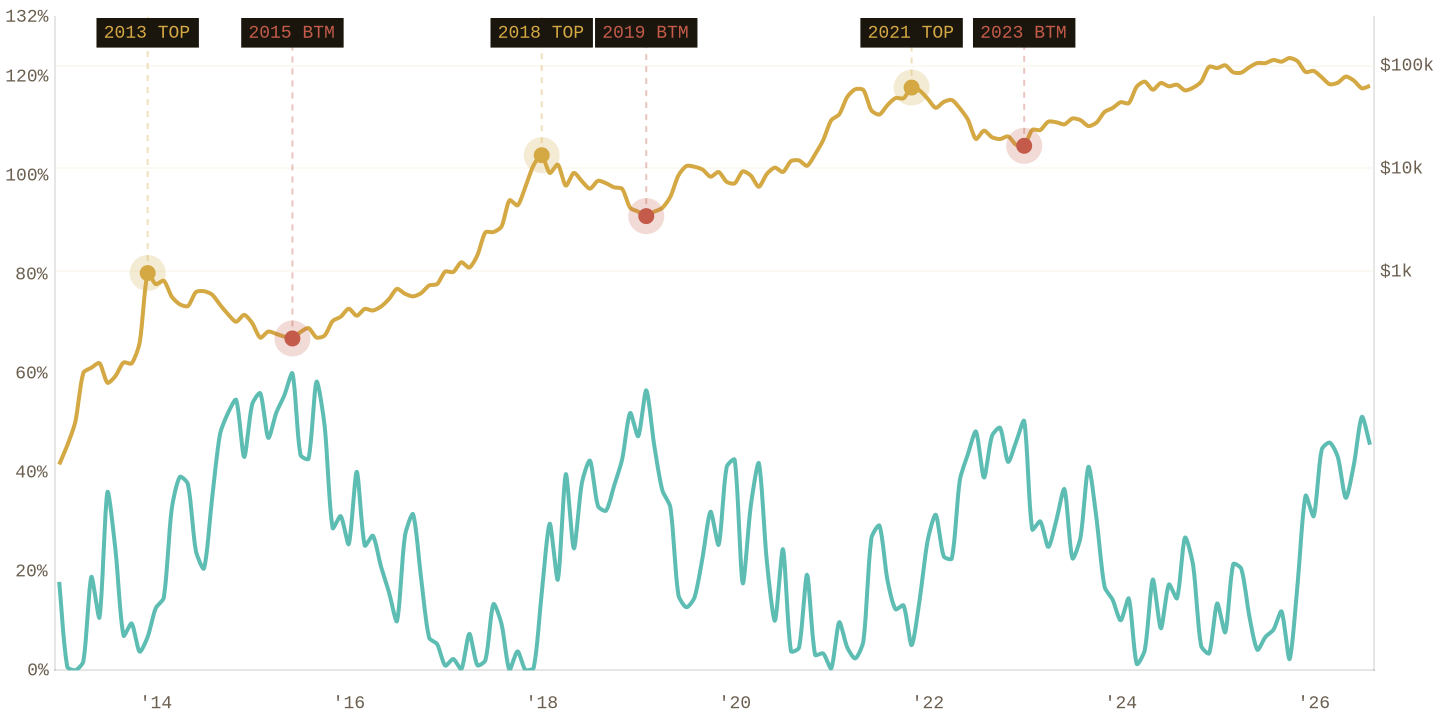

NUPL (Net Unrealized Profit/Loss) measures the aggregate paper profit or loss across all Bitcoin holders. Above zero: the market is in aggregate profit. Below zero: in aggregate loss. Cycle bottoms have historically printed with NUPL deeply negative, essentially the market as a whole holding at a loss.

|

|

BTC Price (log) NUPL

|

|

|

|

BTC Price (log) NUPL

|

|

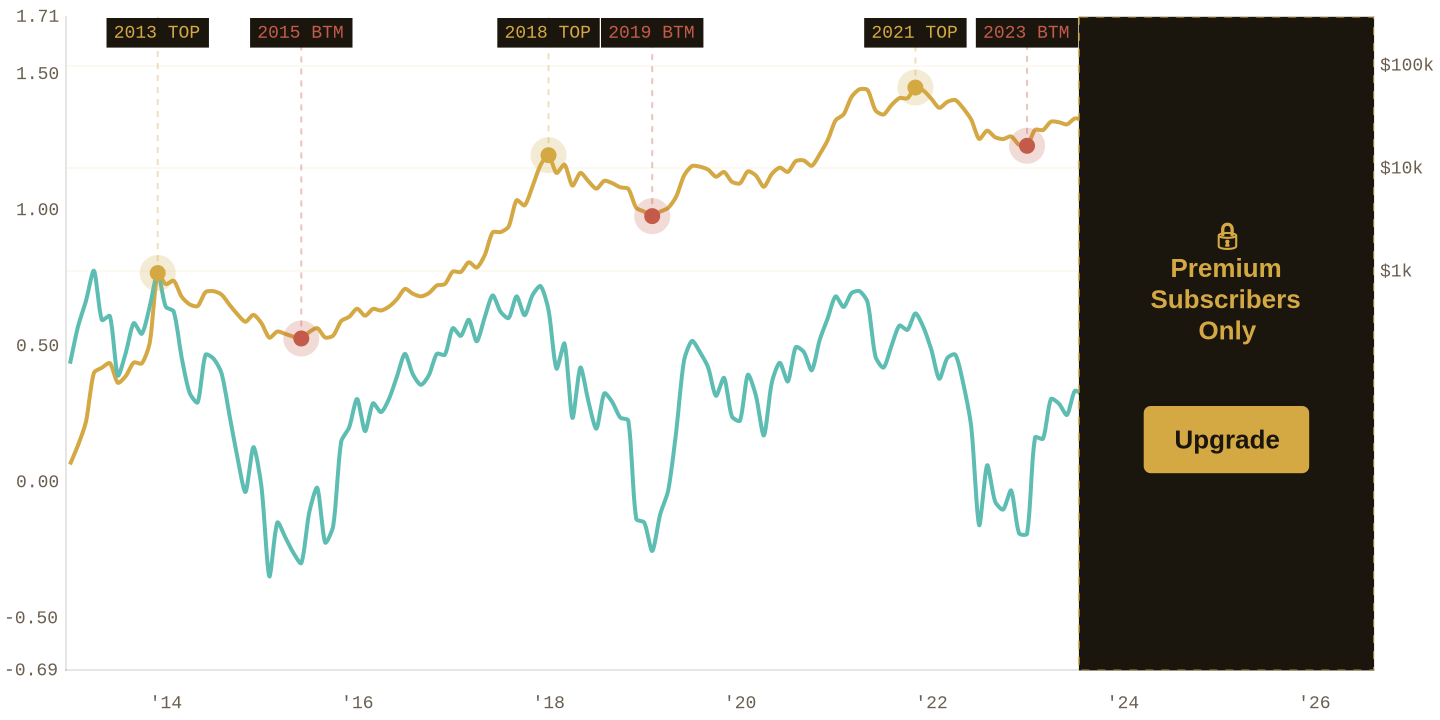

MVRV compares Bitcoin's market cap to its realized cap, essentially spot price divided by realized price. A ratio of 1.0 means the average holder is exactly at break-even. Above 1.0, an aggregate profit. Below 1.0, an aggregate loss. Every cycle bottom in Bitcoin's history has printed MVRV below 1.0.

|

|

BTC Price (log) MVRV ≥ 1 MVRV < 1

|

|

|

|

BTC Price (log) MVRV ≥ 1 MVRV < 1

|

|

AVIV is a realized-value derivative similar in spirit to MVRV but weighted by the active supply (coins that have moved recently). It reads more responsively to short-term positioning shifts than MVRV. Cycle bottoms have shown AVIV compressed well below its long-run average.

|

|

BTC Price (log) AVIV

|

|

|

|

BTC Price (log) AVIV

|

|

The percentage of all Bitcoin held at a profit at the current spot price. At cycle tops this figure has usually run above 90% (essentially nearly every holder was in profit). At cycle bottoms it collapsed to 40–55% (roughly half the network is underwater)

|

|

BTC Price (log) Supply in Profit

|

|

|

|

BTC Price (log) Supply in Profit

|

|

The mirror of the metric above (percentage of all Bitcoin held at a loss). Cycle bottoms have historically seen this rise to 45–60% as capitulation sets in.

|

|

BTC Price (log) Supply in Loss

|

|

|

|

BTC Price (log) Supply in Loss

|

|

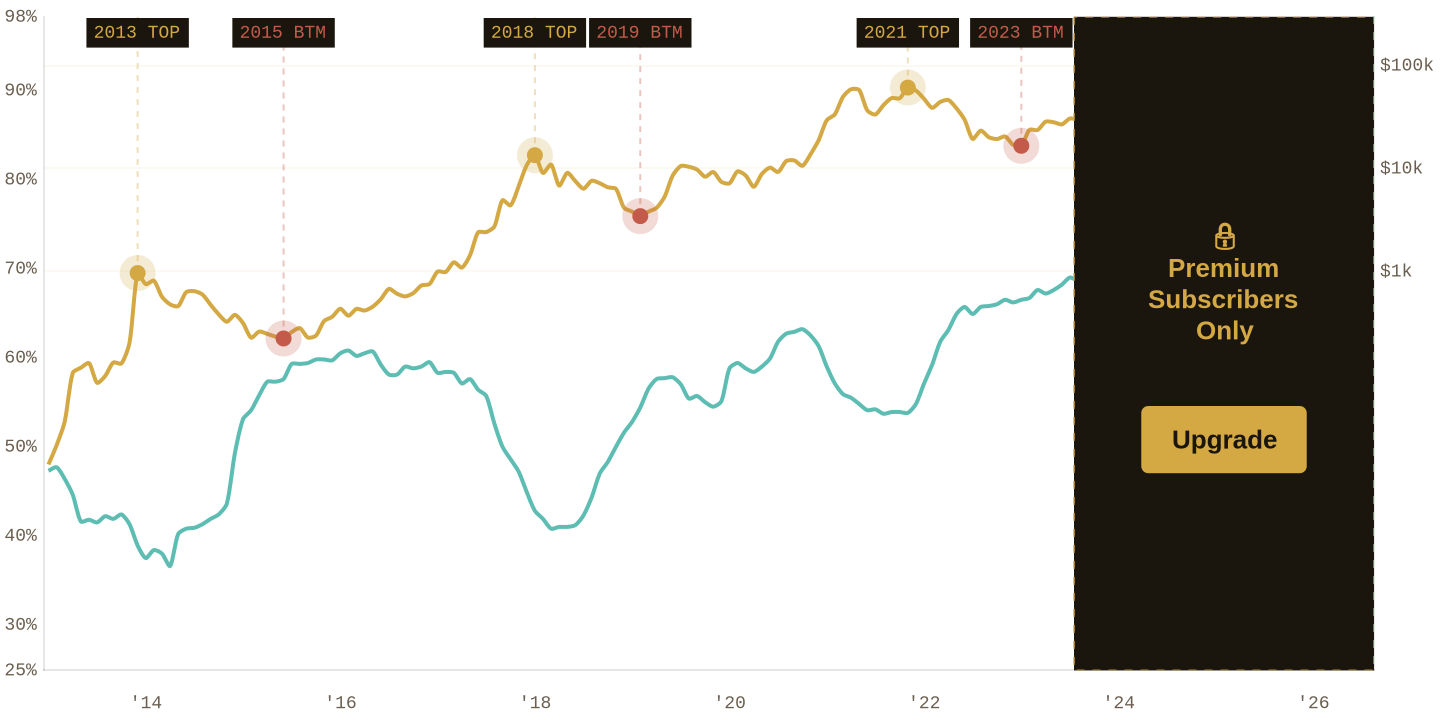

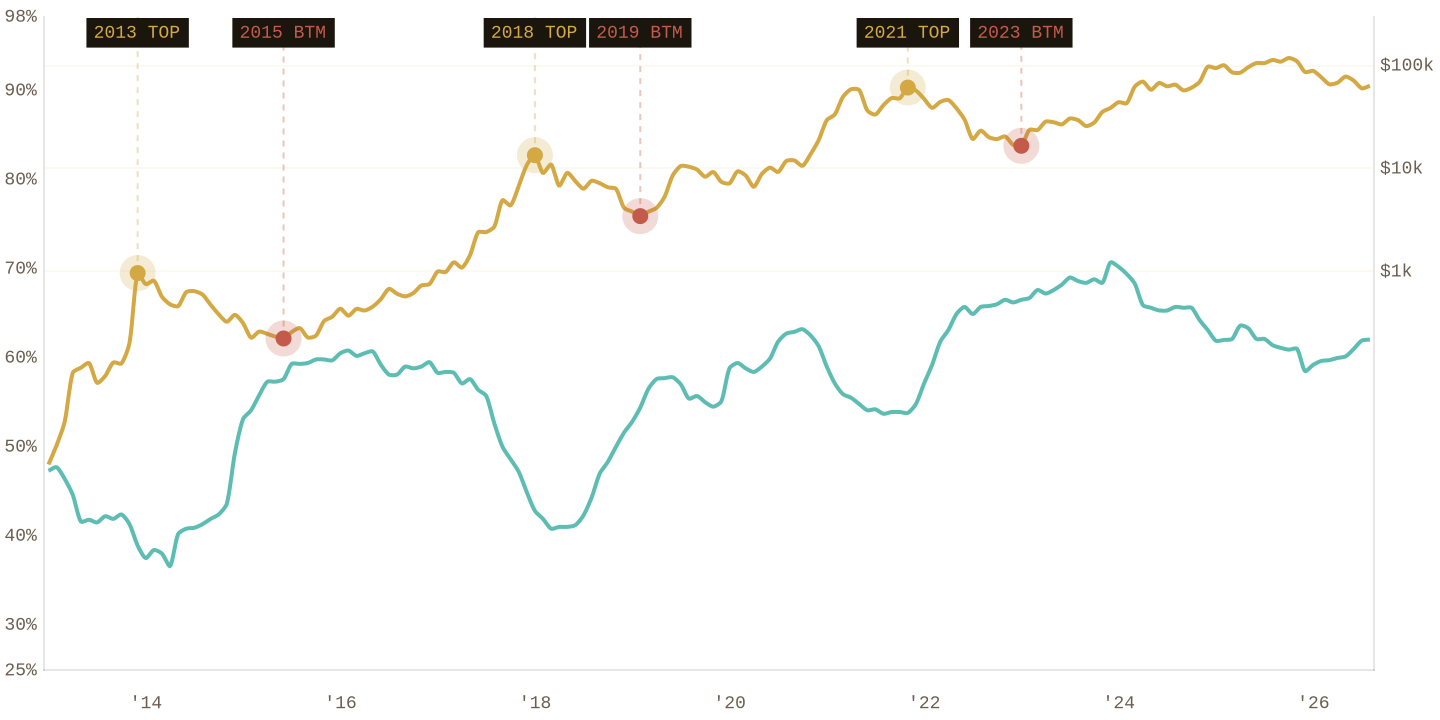

The percentage of circulating Bitcoin that hasn't moved in the last year (a proxy for long-term-holder conviction). As you can see from the chart, the metric entered a divergence between bitcoin price in every single cycle. Tops usually happen when price moves up but the metric goes down (which means long term holders are selling and taking profits as the price makes new high). Bottoms usually happen when price goes down but the metric starts going up (which means people have stopped selling and started accumulating).

|

|

BTC Price (log) HODL 1y+ supply

|

|

|

|

BTC Price (log) HODL 1y+ supply

|

|

Central banks and inflation

The rate-cut narrative that fueled the run to $124k has weakened. Inflation risk hasn't gone away: the ongoing war in Europe keeps energy and commodity prices bid, and central banks (FED, ECB, BOE) are signaling higher for longer rather than aggressive easing. Every cycle top in Bitcoin has coincided with a peak in central-bank easing expectations. Every bottom has coincided with the opposite: hawkish repricing that squeezes long-duration risk assets. We're closer to the hawkish side of that pendulum than the market seems to want to acknowledge.

AI is soaking up the liquidity

The other structural headwind is AI. A meaningful share of the marginal risk-on dollar in 2025 and 2026 has flowed into AI companies (mega-cap platform names, GPU infrastructure, and the private capital chasing the same theme). That capital used to rotate into Bitcoin during risk-on phases. It's now competing with Bitcoin for the same allocation. Even if the FED pivots, we shouldn't assume the "everything rally" of prior cycles repeats.

The long-term trend is intact

None of the above changes the long-term picture. Three things worth remembering as you sit through this drawdown:

Long-term holders keep growing. The share of supply held by wallets that haven't moved in 1+ years is at multi-year highs.

The retail base keeps expanding. The number of addresses holding at least 0.01 BTC is at a new all-time high. Whatever price does short-term, the network is broader today than at any prior point in its history.

Institutions keep buying. New sovereign, state, and public-company allocations are announced almost weekly. This buyer cohort didn't exist in 2018 and barely existed in 2022.

While the current bounce seems more likely a relief rally than the bottom, if you're a long-term holder, that changes nothing as you keep accumulating on drawdowns. If you were about to size up on the "bottom is in" narrative, our dataset isn't confirming that call yet so I wouldn’t do anything crazy (like leveraged trades, etc…)